If you owe a lot of money and find it hard to pay your bills, you might search for a cheap and easy way to clear your debts. People often choose debt settlement to solve their debt problems because it can save more money compared to other methods like debt consolidation, debt management, or even declaring bankruptcy.

Debt settlement companies help by reducing the amount you owe, making it an affordable option for many. So, many believe that debt settlement is the most cost-effective way to get out of debt.

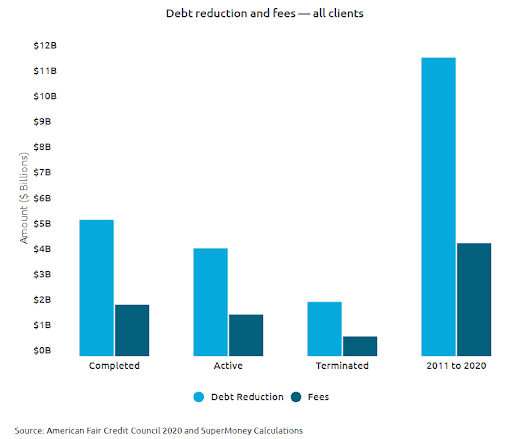

Debt settlement programs may not be the right choice for everyone, but they do help most people save money. A review by Hemming Morse LLP for the American Fair Credit Council (AFCC) showed that 98% of people saved money, even after paying all the fees.

This study examined nearly 12 million accounts and about 1.6 million people using debt settlement programs between 2011 and 2020. These companies only get paid after they successfully settle a debt, ensuring that usually, the savings are more than the costs charged by these services.

The American Fair Credit Council (AFCC) conducted a study that found, on average, clients save $2.64 for every $1 they spend on fees in debt settlement programs. This means that if you save $2.64, you would spend about 38% of those savings ($1) on fees.

In the study from 2011 to 2020, it was observed that clients spent a total of $4.5 billion on fees but could pay off $11.8 billion in debt. These details were illustrated in a chart in the study.

Still, is debt settlement the least expensive way to get out of debt? How about we take a better look and decide?

What does debt settlement mean?

Debt settlement is a way to reduce the money you owe by talking and making deals with the people or companies you owe money to. This is often done through companies that specialize in helping people lower their debts. They work with your creditors to agree on a lower amount for you to pay back. It’s not a free service, and it can be risky.

Sometimes, you might end up paying back only half or less of what you originally owed, but it depends on what your creditors agree to.

How much does it cost to settle your debt?

The cost to settle your debt varies. If you hire a debt settlement company, they will charge you a fee based on the amount of debt reduced. Additionally, there might be extra costs, such as late fees and higher interest rates during the negotiation process. It’s also essential to consider potential tax implications on the settled debt.

All these factors contribute to the overall cost of settling your debt.

Hiring a Company vs. Doing It Yourself:

Settling Independently:

- You can choose to negotiate with creditors on your own, trying to lower the amount you owe without external help.

Using a Debt Settlement Company:

- Hiring a company involves paying a fee, usually based on the amount of debt reduced. Fees typically range from 15% to 25% of the saved money.

Impact on Credit Score:

Initial Drop:

- When you start the debt settlement process, expect your credit score to decrease initially.

Effect of Missed Payments:

- Missing a payment during negotiations could lead to a significant drop in your credit score, similar to the impact of bankruptcy.

Saving Money vs. Credit Score:

Potential Savings:

- Debt settlement might reduce the total debt owed, saving you some money.

Tax Implications:

- The IRS may consider forgiven debts above $600 as taxable income, which could reduce the overall benefit from debt settlement.

Additional Costs and Risks:

Accumulation of Fees:

- During the settlement process, you might accrue late fees and interest, making the debt harder to settle.

Legal Risks:

- Sometimes, creditors might sue for unpaid debts, especially those over $5,000. This can lead to wage garnishments.

Creditor Approval:

Creditor’s Willingness:

- Not all creditors are open to negotiation with debt settlement companies. Some prefer direct interaction with borrowers.

Specific Creditor Policies:

- Companies like Chase, for example, prefer dealing directly with consumers or accredited non-profit credit counseling agencies.

Uncertainties:

No Guarantees:

- There’s no certainty in debt settlement negotiations; creditors might not agree to reduce the owed amount.

Possible Increase in Costs:

- If debts aren’t substantially reduced, the increased costs due to interest and fees might offset the savings from settled debts.

Debt settlement vs debt consolidation

When dealing with multiple debts, you might settle your debt or consolidate it. However, it’s crucial to understand the differences and risks associated with each option.

Debt Settlement:

What It Is:

- Debt settlement companies offer to negotiate with your creditors to reduce the total amount you owe.

- They manage your debt accounts, collect payments, and then make lump-sum settlement offers to creditors.

Risks and Costs:

- This option can lower your credit score, accumulate late fees and interests, and even risk legal actions from creditors.

- The associated fees, including enrollment and maintenance charges, can be substantial, sometimes up to 60% of the enrolled debt.

Debt Consolidation:

What It Is:

- Unlike debt settlement, this involves combining various debts into a single payment.

- Methods include balance transfer credit cards and debt consolidation loans, aiming to make repayment more manageable.

Rates and Fees:

- Each method comes with specific rates, fees, and eligibility criteria.

- The objective is to reduce interest rates, make payments more manageable, and shorten repayment periods.

- Different methods come with varied rates and fees, like a 3-5% fee for balance transfers.

- Loan origination fees range from 1% to 8%.

DIY Approaches:

Self-Management:

- Managing and consolidating debts on your own can save you from additional costs, unlike hiring a debt settlement company.

Comparison:

Interest Rates and Fees:

- Debt consolidation aims to lower your expenses, while debt settlement might incur additional costs, like late fees and higher interest rates.

Credit Score Impact:

- Consolidating debts usually doesn’t harm your credit score, but settling debts can significantly lower it.

Knowing these differences and considerations can help you make an informed decision about whether to settle or consolidate your debts based on your financial situation and goals.

Debt settlement vs credit counseling and debt management plan

Navigating through financial hardships requires a careful choice between various debt relief options. Let’s dive deeper into understanding debt settlement and credit counseling with a debt management plan (DMP).

Debt Settlement:

Cost and Impact on Credit:

- Debt settlement generally comes with substantial fees.

- It quickly reduces the owed amount but severely impacts your credit score, making future loans more expensive.

Operational Strategy:

- Companies negotiate with your creditors to lower the amount you owe.

- They often advise stopping payments to creditors during negotiations, attracting additional risks and penalties.

Risks:

- Some companies may operate unscrupulously, so due diligence is advised.

- Direct negotiations with creditors might be a safer initial approach.

Credit Counseling and DMP:

Sustainability:

- It is ideal for those managing a strict monthly budget, ensuring consistent payment towards debts.

Effect on Finances:

- Run by non-profit entities, they usually offer reasonable fees and maintain your credit score by ensuring debts are paid off in full.

Holistic Approach:

- These agencies provide comprehensive guidance, including budgeting advice and strategies for effective financial management.

Negotiation and Planning:

- They collaborate with creditors to lower interest rates and waive off certain fees, ensuring that repayment becomes more manageable.

Comparative Summary:

Impact on Financial Health:

- While debt settlement provides a quicker resolution, it carries higher risks and more considerable damage to your credit score.

- Credit counseling with a DMP, though longer, provides a structured path to debt freedom with minimal impact on your credit score and more holistic financial guidance.

Understanding each approach’s detailed implications will allow for a choice that aligns best with your financial goals and capabilities.

Debt Settlement vs. Bankruptcy: Making The Right Choice

Navigating through financial hardships involves making crucial decisions. Understanding the differences between debt settlement and bankruptcy is essential to make a choice that suits your financial situation best.

Debt Settlement:

Flexibility: It’s more adaptable, fitting those with temporary financial struggles due to situations like job loss or medical expenses.

Duration: It takes a few years and appears on credit records for seven years, but it’s typically shorter than bankruptcy.

Impact on Credit: It does affect credit scores but is less severe compared to the implications of bankruptcy.

Process:

- Debt settlement companies negotiate with creditors to reduce the total debt owed.

- There are fees involved, paid to the debt settlement companies.

Bankruptcy:

Types and Processes:

- Chapter 7: Quick resolution (3-6 months), but assets might be sold off to pay creditors.

- Chapter 13: Involves a 3-5 year payment plan, allowing retention of assets like houses.

Eligibility:

- Not everyone qualifies; eligibility depends on income levels and other factors.

Impact on Credit and Job Prospects:

- It severely affects credit scores, staying on records for up to 10 years.

- It may limit job opportunities as some employers consider credit history.

Legal Protection:

- Offers protection against lawsuits and creditor harassment, unlike debt settlement.

Comparison:

Completion Time: Bankruptcy, especially Chapter 7, is usually quicker but has a more extended impact on credit.

Legal Fees:

- Bankruptcy involves attorney fees and filing charges, making it expensive.

- Debt settlement comes with service fees but might be more affordable.

Effect on Life and Employment:

- Bankruptcy might bring immediate relief but can have a longer-lasting impact on personal life and job prospects.

Choosing between debt settlement and bankruptcy depends on individual circumstances, the urgent relief required, and the willingness to bear the long-term impacts.

Both paths offer ways out of financial distress but come with different costs, benefits, and consequences. Understanding these aspects thoroughly ensures a decision that aligns with personal financial recovery goals.

Tax Implications of Debt Settlements

When considering debt settlement, it’s crucial to comprehend the tax implications fully. Here’s a breakdown to guide you through the complexities of debts and taxes.

Taxation on Settled Debts:

Taxable Income: The IRS considers forgiven debt above $600 as additional income, which is taxable.

Determining Your Taxes:

- Tax Brackets: Your total income, including forgiven debt, will fall into specific tax brackets ranging from 10% to 37%.

- Form 1099-C: This form indicates the amount of forgiven debt and is shared with the IRS to track your income.

Calculating Taxes on Forgiven Debts:

Consider Your Overall Income:

- Taxes depend on your total income, which affects the tax bracket you fall into.

- Forgiven debts will be added to your income and taxed at the corresponding rate.

Influence on Tax Liability:

- Tax Credits and Deductions: Having tax benefits might help reduce taxable income and, subsequently, the taxes on forgiven debts.

- Potential Shift in Tax Brackets: An increased reported income due to forgiven debts might shift you to a higher tax bracket, leading to increased taxes.

Special Considerations:

- Exclusions: In certain situations, like bankruptcy or insolvency, you might be exempt from taxes on forgiven debts.

Reporting and Compliance:

- IRS Audits: Not reporting forgiven debts may result in IRS audits, leading to additional taxes, penalties, and interest.

While debt settlement can offer relief, understanding its tax implications is vital. Ensure that all forgiven debts are accurately reported to avoid potential complications with the IRS, and consider consulting a tax professional to navigate the specific nuances of your financial situation effectively.

Conclusion

Debt settlement is a strategic option for managing substantial unsecured debts, offering a potential pathway to financial stability. Before proceeding, it’s crucial to explore all alternatives and consult professionals like credit counselors and bankruptcy attorneys to make an informed decision.

Ensuring collaboration with a reputable debt settlement company is also vital to avoid potential scams and ensure a secure, reliable partnership in the journey toward financial liberation. Careful consideration of various factors, including hidden fees and overall interest payments, is necessary to navigate the complexities of debt settlement effectively.

About the Author:

Lyle Solomon has extensive legal experience, in-depth knowledge, and experience in consumer finance and writing. He has been a member of the California State Bar since 2003. He graduated from the University of the Pacific’s McGeorge School of Law in Sacramento, California, in 1998 and currently works for the Oak View Law Group in California as a principal attorney.